Gov/Mil: Optical Satcom Ignitor or Propellant?

Government and military customers have been at the epicentre of demand for optical satellite communications as it transitions from nascent and equipment-centric to a robust emerging ecosystem. Organizations such as SDA, DARPA have been key facilitators for this move through multiple contracts for their planned Tranche 0, Tranche 1 and Blackjack constellations, and research programs that enable further technology development. One question arises: is this demand an ignitor or propellant of the optical satcom market?

Market Opportunity

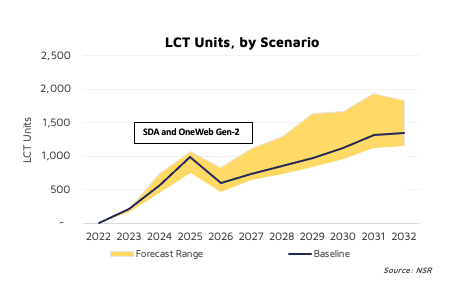

NSR’s Optical Satellite Communications, 5th Edition forecasts total market demand of 8,600+ LCT Units during the 2022-2032 period. There is spike in demand in the short term, mostly driven by Gov/Mil. customers such as SDA who have planned satellites with optical intersatellite links for Transport Layer Tranche 0 and Tranche 1 as part of the Proliferated Warfighter Space Architecture (PWSA, formerly known as National Defense Space Architecture (NDSA)). The convergence of SDA launches, and OneWeb Gen-2 constellation launches results in a peak in 2025. The start of launches by data relay operators adds to the demand in 2024 and 2025 as well. The potential growth is gradual post 2025 corresponding to growth in Gen-2 communication constellation launches.

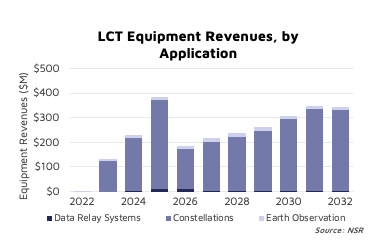

The revenue generated during the decade is $2.6 B, growing at CAGR of 67.3%, nourished by additions of units sold. However, the increase in units is coupled with a decrease in pricing over the timeline resulting in the lower equipment revenues towards the end of the decade. Most revenues are driven by Communications followed by Earth Observation applications. The market opportunity is primarily driven by optical inter-satellite links for all the applications due to larger adoption by mega-constellation operators.

Security, A Fundamental for Gov/Mil

Optical satellite communications have multiple advantageous factors such as higher data rates, larger bandwidth, and lower SWaP requirements that increase the adoption of optical terminals. However, security is the most vital factor that attracts the demand from Gov/Mil customers. Higher security is inherent with utilizing optical communications as it is immune to interception and jamming. Optical has lower beam spread compared to RF, which makes it difficult to intercept and difficult for ground-based threats to communicate with satellite in-orbit. Jamming of optical link is far more challenging compared to RF due to high precision targeting requirements by receiver to obstruct communications traffic. Thus, it has attracted the attention of several customers and is the reason why it has received increased funding by Gov/Mil players. For example, EU member States have tentatively agreed to cover costs up to 2.4 billion euros for IRIS2 network (Infrastructure for Resilience, Interconnectivity and Security by Satellite), which will feature optical links.

Gov/Mil Enabling the Ecosystem

The Gov/Mil segment has been a key enabler for the optical satellite communication ecosystem through contracts for optical terminals for Tranche 0 and Tranche 1 satellites, as noted above. Mynaric, SA Photonics, Skyloom and Tesat are now suppliers of OISLs for SDA’s tranche 0. In addition, constellation operators such Amazon’s Kuiper, and Capella Space will utilise SDA compatible OISLs as part of their constellation.

The adoption of OISLs is expected to grow for faster data delivery, and SDA compatible LCTs will enable direct data delivery to military customers at desired location through their own mesh network. However, the adoption of LCTs for inter-satellite links and DTE terminals is still limited to existing cheaper RF terminals. Thus, the Gov/Mil segment does play an instrumental role in increasing adoption of OISLs across the satellite operators who focus on Defence and Intelligence applications. This trend is expected to pick up for other data sets such as environmental monitoring, forest monitoring applications where the major customer is Government organizations.

Another way Gov/Mil is influential is through R&D contracts for technology development. Companies such as Space Micro are working on the development of GEO terminals for the U.S. Space Force and Optical RF converters which will enhance their product offering. Also, these contracts enhance the applications where LCTs will be implemented, for example in space-to-air communications (aircrafts/UAVs). These contracts are enabling and setting the future roadmap for the industry players.

Interoperability: The Next Frontier

In this context, interoperability is becoming essential to create the “internet of satellites”; i.e., seamless communication across Gov/Mil and commercial satellites. DARPA is behind the research on interoperability through its Space-Based Adaptive Communications Node (Space-BACN) program. The main objective of the program is to develop low-cost, high-speed, re-configurable optical datalinks to connect LEO constellations. The inter-operable terminals will enable different data rate systems/constellations to communicate: 2.5 Gbps networks can communicate with a 10 Gbps network by adapting to lowest data rate in the linked satellites across constellations. This will allow cross constellation communication to downlink data or operate necessary sensors in the least time possible, which is a required capability for many Gov/Mil applications.

The vision for the program is to fit into overall system architecture enabling mosaic warfare capabilities. There is a shift towards COCO-GO (Contractor Owned Contractor Operated(maintenance) Government Operated (Use)) model from GOGO (Government Owned Government Operated) model through the program, which will enable commercial players to offer services on a pay-as-you-go basis. Thus, this facilitates further service opportunities for commercial constellation operators, which in-turn increases the potential of adoption of OISLs by communication satellite operators.

In addition, the Space-BACN program is facilitating the optical ecosystem by funding their R&D phases or reducing the cost of NRE for their planned products. This addresses the challenge the new space players face; i.e., higher NRE costs which can lead to higher cost per terminal. Companies such as CACI, mBryonics and Mynaric are working on TA1, Intel along with II-VI Aerospace and Arizona state university on TA2 and SpaceX, Telesat, SpaceLink, Viasat and Kuiper Government Solutions LLC for TA3. The 3 Technical Areas(TA) are for the development of optical heads responsible for Pointing Acquisition and Tracking (PAT), the second is design of reconfigurable modems, and the third is identification of critical command and control elements for cross constellation OISL communications.

This supports the key equipment manufacturers to develop technological capabilities at lower cost. The target price point as per the program is $100K per terminal, which is much lower compared to current terminal costs in the market, enabling the players to leverage the output of program to position low-cost product in the market, which will strengthen their value proposition. NSR expects interoperability to provide an “edge” to service providers targeting the Gov/Mil customer segment.

SDA Driving Standardization

The lack of standardization across terminals has been a key challenge in the market, due to a very large and diverse offering. However, SDA’s Optical Communication Terminal (OCT) Standard (Version 3.0) has gradually been adopted by a majority of key market players. These standards offer interface specifications to facilitate interoperability of spacecrafts via OISLs coupled with integration with SDA’s Transport Layer. NSR expects gradual expansion on SDA standards to be adopted as international standards for OISLs in the long-term. Thus, Gov/Mil segment will continue to be an enabler for market growth and market establishment.

The Bottom Line

In the short term, a major portion of opportunity will come from the Gov/Mil segment, which has enabled the market ecosystem and initiated the market to be an easier addressable opportunity for commercial players. Additionally, the Gov/Mil segment has been a catalyst by providing standards, sponsoring the research and development of new technologies that will eventually boost optical communications' capabilities and demand. Thus, the Gov/Mil segment is both a ignitor and propellant for optical satellite communications.

Author

Prachi Kawade

Senior Analyst, expert in space and satelliteRelated items

Article

Players in the satellite-based Earth observation market must target government analytics procurement

Forecast report

Global space economy: trends and forecasts 2023–2033

Forecast report

Lunar market: trends and forecasts 2024–2034